I’d consider some creative sourcing for used homes that fit your criteria… Bandit signs, Facebook posts, Craigslist, or even direct mail using the state mobile home registration data (if it’s public in your state). Focus on areas where the 30# requirement is in force.

You can probably get some small bird dog fees for the 20# load homes you can’t use from some operators further south to at least cover your advertising costs, or get some favors and goodwill from other operators.

I have done the registration mailouts before - my response rate was all over the place because I made bad assumptions on my data filters…but it’s doable. Did not go again because I can still find cheap homes that I can move from 3-4 hours from where I operate…

“…I have been considering a plan to purchase new homes through the Cash Program’s Community Owned program or other lender groups of homes at a time to rent out…”

The CASH Program has been around since 2012 and has had multiple revisions in the details.

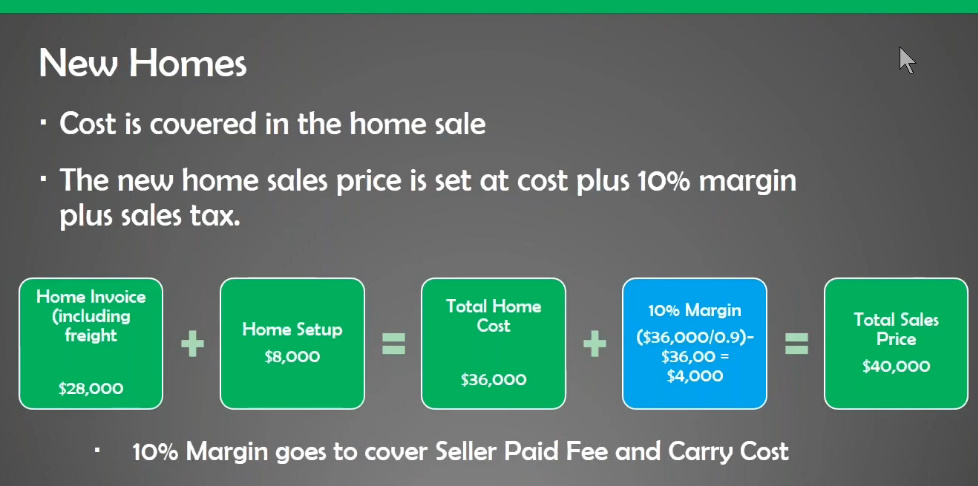

As per one of the CASH Slides (screen shot below):

“New Homes”

“Cost is covered in the home sale”

“Home Invoice (including freight) + Home Setup = Total Home Cost + 10% Margin = Total Sales Price”

My concern with the CASH Program is:

What liability/responsibility is the Mobile Home Park Owner signing up for IF the New Home is repossessed?

As per another of the CASH Slides (screen shot below):

Repo Homes: “Operator purchases repossessed home for payoff (tiered 65% to 90%)…”

When the Home is repossessed and the “Loan” includes all these Fees (Freight & Setup & Margin), will the “Payoff” be more than the value of the Home?

What IF the Mobile Home Park needs to be sold BEFORE the Homes are sold or paid off? Will other potential MHP Buyers desire to take over the Liability/Responsibility of the CASH Loans?

Almost certainly yes. Even with zero fees, but even more so with fees, the homeowner is underwater until nearly the payoff because the depreciation is catching up with the amortization of the retail price, which is already approximately double the wholesale or repo “value.” Generally. That is the lenders risk which is baked into the interest rate of creditworthiness risk/return ratio.

But 21st is charging customer-risk default interest rates with park-owner type credit risk which is really just heaping it on the homeowner because that’s the market rate of interest the borrower can expect. If you’re a good borrower with bad credit, 21st makes a bundle on interest. If you’re a bad borrower who defaults, 21st loses nothing because the park owner is on the hook. Heads they win, tails you lose.